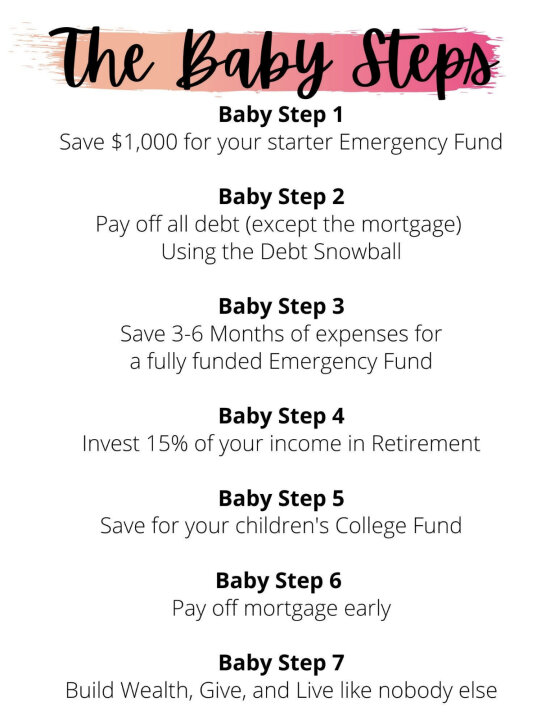

When I was younger I got in over my head with credit card debt, at some point you just have to stop spending and pay the bills. After taking a few years of real work to pay them off, I started putting money in savings instead of spending it. I travel for work and have 2 cards I use for that, they never go more than 30 days without being at a zero balance. Check out a guy named Dave Ramsey, he has a program called The Money Make over. I have a few friends that it has worked for. You will never be wealthy if you spend more than you make.